The emission rights trading is an administrative tool used to control greenhouse gas emissions . These rights have 5 years of validity.

A central authority (usually a government or an international organization) sets a limit on the amount of polluting gases that can be emitted. Companies are obliged to manage a number of bonds (also known as rights or credits), which represent the right to issue a certain amount of waste. Companies that need to increase emissions above their limit should buy credits from other companies that pollute below the limit that marks the number of credits that have been granted. The transfer of credits is understood as a purchase. In effect, the buyer is paying an amount of money for polluting, while the seller is rewarded for having managed to reduce their emissions. In this way, it is achieved, in theory, that the companies that make effective the reduction of emissions are those that do so more efficiently (at lower cost), minimizing the added bill that the industry pays to achieve the reduction.

There are programs of rights trading for various types of pollutant. For greenhouse gases, the most important one is the European Union Emission Rights Trade Regime (EU ETS). In the United States there is a national market for the reduction of acid rain and several regional markets for nitrogen oxides . Markets for other pollutants tend to be smaller and more localized.

Trade in emission rights is seen as a more efficient approach than charging or direct regulation. It can be cheaper, and politically more desirable for existing industries, for which the granting of permits is made with certain exemptions proportional to historical emissions. In addition, most of the money generated by this system goes to environmental activities. Criticism of emissions trading is based on the difficulty of controlling all the activities of the industry and assigning the initial rights to each company.

Trade

To understand carbon trading, it is important to understand the products that are being traded. The primary product in carbon markets is the trading of GHG emission permits. Under a cap-and-trade system, permits are issued to various entities for the right to emit GHG emissions that meet emission reduction requirement caps.

One of the controversies about carbon mitigation policy is how to “level the playing field” with border adjustments. For example, one component of the American Clean Energy and Security Act (a 2009 bill that did not pass), along with several other energy bills put before US Congress, calls for carbon surcharges on goods imported from countries without cap-and-trade programs. Besides issues of compliance with the General Agreement on Tariffs and Trade, such border adjustments presume that the producing countries bear responsibility for the carbon emissions.

A general perception among developing countries is that discussion of climate change in trade negotiations could lead to “green protectionism” by high-income countries (World Bank, 2010, p. 251). Tariffs on imports (“virtual carbon”) consistent with a carbon price of $50 per ton of CO2 could be significant for developing countries. World Bank (2010) commented that introducing border tariffs could lead to a proliferation of trade measures where the competitive playing field is viewed as being uneven. Tariffs could also be a burden on low-income countries that have contributed very little to the problem of climate change.

Trading systems

Kyoto Protocol

In 1990, the first Intergovernmental Panel on Climate Change (IPCC) report highlighted the imminent threat of climate change and greenhouse gas emission, and diplomatic efforts began to find an international framework within which such emissions could be regulated. In 1997 the Kyoto Protocol was adopted. The Kyoto Protocol is a 1997 international treaty that came into force in 2005. In the treaty, most developed nations agreed to legally binding targets for their emissions of the six major greenhouse gases. Emission quotas (known as “Assigned amounts”) were agreed by each participating ‘Annex I’ country, with the intention of reducing the overall emissions by 5.2% from their 1990 levels by the end of 2012. Between 1990 and 2012 the original Kyoto Protocol parties reduced their CO2 emissions by 12.5%, which is well beyond the 2012 target of 4.7%. The United States is the only industrialized nation under Annex I that has not ratified the treaty, and is therefore not bound by it. The IPCC has projected that the financial effect of compliance through trading within the Kyoto commitment period will be limited at between 0.1-1.1% of GDP among trading countries. The agreement was intended to result in industrialized countries’ emissions declining in aggregate by 5.2 percent below 1990 levels by the year of 2012. Despite the failure of the United States and Australia to ratify the protocol, the agreement became effective in 2005, once the requirement that 55 Annex I (predominantly industrialized) countries, jointly accounting for 55 percent of 1990 Annex I emissions, ratify the agreement was met.

The Protocol defines several mechanisms (“flexible mechanisms”) that are designed to allow Annex I countries to meet their emission reduction commitments (caps) with reduced economic impact.

Under Article 3.3 of the Kyoto Protocol, Annex I Parties may use GHG removals, from afforestation and reforestation (forest sinks) and deforestation (sources) since 1990, to meet their emission reduction commitments.

Annex I Parties may also use International Emissions Trading (IET). Under the treaty, for the 5-year compliance period from 2008 until 2012, nations that emit less than their quota will be able to sell assigned amount units (each AAU representing an allowance to emit one metric tonne of CO2) to nations that exceed their quotas. It is also possible for Annex I countries to sponsor carbon projects that reduce greenhouse gas emissions in other countries. These projects generate tradable carbon credits that can be used by Annex I countries in meeting their caps. The project-based Kyoto Mechanisms are the Clean Development Mechanism (CDM) and Joint Implementation (JI). There are four such international flexible mechanisms, or Kyoto Mechanism, written in the Kyoto Protocol.

Article 17 if the Protocol authorizes Annex 1 countries that have agreed to the emissions limitations to take part in emissions trading with other Annex 1 Countries.

Article 4 authorizes such parties to implement their limitations jointly, as the member states of the EU have chosen to do.

Article 6 provides that such Annex 1 countries may take part in joint initiatives (JIs) in return for emissions reduction units (ERUs) to be used against their Assigned Amounts.

Art 12 provides for a mechanism known as the clean development mechanism (CDM), under which Annex 1 countries may invest in emissions limitation projects in developing countries and use certified emissions reductions (CERs) generated against their own Assigned Amounts.

The CDM covers projects taking place in non-Annex I countries, while JI covers projects taking place in Annex I countries. CDM projects are supposed to contribute to sustainable development in developing countries, and also generate “real” and “additional” emission savings, i.e., savings that only occur thanks to the CDM project in question (Carbon Trust, 2009, p. 14). Whether or not these emission savings are genuine is, however, difficult to prove (World Bank, 2010, pp. 265–267).

Australia

In 2003 the New South Wales (NSW) state government unilaterally established the NSW Greenhouse Gas Abatement Scheme to reduce emissions by requiring electricity generators and large consumers to purchase NSW Greenhouse Abatement Certificates (NGACs). This has prompted the rollout of free energy-efficient compact fluorescent lightbulbs and other energy-efficiency measures, funded by the credits. This scheme has been criticised by the Centre for Energy and Environmental Markets (CEEM) of the UNSW because of its lack of effectiveness in reducing emissions, its lack of transparency and its lack of verification of the additionality of emission reductions.

Both the incumbent Howard Coalition government and the Rudd Labor opposition promised to implement an emissions trading scheme (ETS) before the 2007 federal election. Labor won the election, with the new government proceeding to implement an ETS. The government introduced the Carbon Pollution Reduction Scheme, which the Liberals supported with Malcolm Turnbull as leader. Tony Abbott questioned an ETS, saying the best way to reduce emissions is with a “simple tax”. Shortly before the carbon vote, Abbott defeated Turnbull in a leadership challenge, and from there on the Liberals opposed the ETS. This left the government unable to secure passage of the bill and it was subsequently withdrawn.

Julia Gillard defeated Rudd in a leadership challenge and promised not to introduce a carbon tax, but would look to legislate a price on carbon when taking the government to the 2010 election. In the first hung parliament result in 70 years, the government required the support of crossbenchers including the Greens. One requirement for Greens support was a carbon price, which Gillard proceeded with in forming a minority government. A fixed carbon price would proceed to a floating-price ETS within a few years under the plan. The fixed price lent itself to characterisation as a carbon tax and when the government proposed the Clean Energy Bill in February 2011, the opposition claimed it to be a broken election promise.

The bill was passed by the Lower House in October 2011 and the Upper House in November 2011. The Liberal Party vowed to overturn the bill if elected. The bill thus resulted in passage of the Clean Energy Act, which possessed a great deal of flexibility in its design and uncertainty over its future.

The Liberal/National coalition government elected in September 2013 has promised to reverse the climate legislation of the previous government. In July 2014, the carbon tax was repealed as well as the Emissions Trading Scheme (ETS) that was to start in 2015.

New Zealand

The New Zealand Emissions Trading Scheme (NZ ETS) is a partial-coverage all-free allocation uncapped highly internationally linked emissions trading scheme. The NZ ETS was first legislated in the Climate Change Response (Emissions Trading) Amendment Act 2008 in September 2008 under the Fifth Labour Government of New Zealand and then amended in November 2009 and in November 2012 by the Fifth National Government of New Zealand.

The NZ ETS covers forestry (a net sink), energy (43.4% of total 2010 emissions), industry (6.7% of total 2010 emissions) and waste (2.8% of total 2010 emissions) but not pastoral agriculture (47% of 2010 total emissions). Participants in the NZ ETS must surrender two emissions units (either an international ‘Kyoto’ unit or a New Zealand-issued unit) for every three tonnes of carbon dioxide equivalent emissions reported or they may choose to buy NZ units from the government at a fixed price of NZ$25.

Individual sectors of the economy have different entry dates when their obligations to report emissions and surrender emission units take effect. Forestry, which contributed net removals of 17.5 Mts of CO2e in 2010 (19% of NZ’s 2008 emissions,) entered the NZ ETS on 1 January 2008. The stationary energy, industrial processes and liquid fossil fuel sectors entered the NZ ETS on 1 July 2010. The waste sector (landfill operators) entered on 1 January 2013. Methane and nitrous oxide emissions from pastoral agriculture are not included in the NZ ETS. (From November 2009, agriculture was to enter the NZ ETS on 1 January 2015)

The NZ ETS is highly linked to international carbon markets as it allows the importing of most of the Kyoto Protocol emission units. However, as of June 2015, the scheme will effectively transition into a domestic scheme, with restricted access to international Kyoto units (CERs, ERUs and RMUs). The NZ ETS has a domestic unit; the ‘New Zealand Unit’ (NZU), which is issued by free allocation to emitters, with no auctions intended in the short term. Free allocation of NZUs varies between sectors. The commercial fishery sector (who are not participants) have a free allocation of units on a historic basis. Owners of pre-1990 forests have received a fixed free allocation of units. Free allocation to emissions-intensive industry, is provided on an output-intensity basis. For this sector, there is no set limit on the number of units that may be allocated. The number of units allocated to eligible emitters is based on the average emissions per unit of output within a defined ‘activity’. Bertram and Terry (2010, p 16) state that as the NZ ETS does not ‘cap’ emissions, the NZ ETS is not a cap and trade scheme as understood in the economics literature.

Some stakeholders have criticized the New Zealand Emissions Trading Scheme for its generous free allocations of emission units and the lack of a carbon price signal (the Parliamentary Commissioner for the Environment), and for being ineffective in reducing emissions (Greenpeace Aotearoa New Zealand).

The NZ ETS was reviewed in late 2011 by an independent panel, which reported to the Government and public in September 2011.

European Union

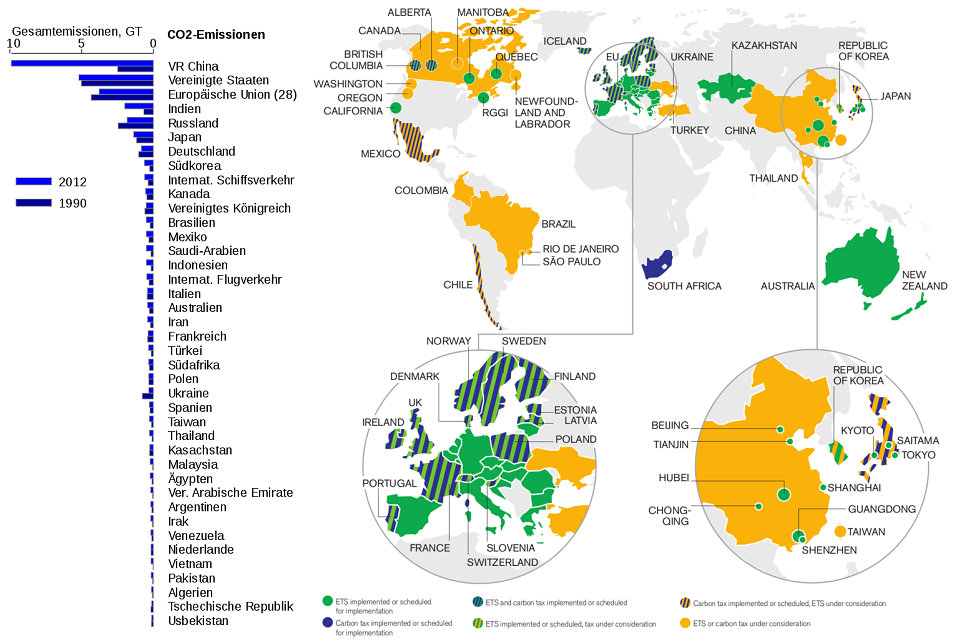

The European Union Emission Trading Scheme (or EU ETS) is the largest multi-national, greenhouse gas emissions trading scheme in the world. It is one of the EU’s central policy instruments to meet their cap set in the Kyoto Protocol.

After voluntary trials in the UK and Denmark, Phase I began operation in January 2005 with all 15 member states of the European Union participating. The program caps the amount of carbon dioxide that can be emitted from large installations with a net heat supply in excess of 20 MW, such as power plants and carbon intensive factories and covers almost half (46%) of the EU’s Carbon Dioxide emissions. Phase I permits participants to trade among themselves and in validated credits from the developing world through Kyoto’s Clean Development Mechanism. Credits are gained by investing in clean technologies and low-carbon solutions, and by certain types of emission-saving projects around the world to cover a proportion of their emissions.

During Phases I and II, allowances for emissions have typically been given free to firms, which has resulted in them getting windfall profits. Ellerman and Buchner (2008) suggested that during its first two years in operation, the EU ETS turned an expected increase in emissions of 1%-2% per year into a small absolute decline. Grubb et al. (2009) suggested that a reasonable estimate for the emissions cut achieved during its first two years of operation was 50-100 MtCO2 per year, or 2.5%-5%.

A number of design flaws have limited the effectiveness of the scheme. In the initial 2005-07 period, emission caps were not tight enough to drive a significant reduction in emissions. The total allocation of allowances turned out to exceed actual emissions. This drove the carbon price down to zero in 2007. This oversupply was caused because the allocation of allowances by the EU was based on emissions data from the European Environmental Agency in Copenhagen, which uses a horizontal activity-based emissions definition similar to the United Nations, the EU ETS Transaction log in Brussels, but a vertical installation-based emissions measurement system. This caused an oversupply of 200 million tonnes (10% of market) in the EU ETS in the first phase and collapsing prices.

Phase II saw some tightening, but the use of JI and CDM offsets was allowed, with the result that no reductions in the EU will be required to meet the Phase II cap. For Phase II, the cap is expected to result in an emissions reduction in 2010 of about 2.4% compared to expected emissions without the cap (business-as-usual emissions). For Phase III (2013–20), the European Commission proposed a number of changes, including:

Setting an overall EU cap, with allowances then allocated t

Tighter limits on the use of offsets;

Unlimited banking of allowances between Phases II and III;

A move from allowances to auctioning.

In January 2008, Norway, Iceland, and Liechtenstein joined the European Union Emissions Trading System (EU ETS), according to a publication from the European Commission. The Norwegian Ministry of the Environment has also released its draft National Allocation Plan which provides a carbon cap-and-trade of 15 million metric tonnes of CO2, 8 million of which are set to be auctioned. According to the OECD Economic Survey of Norway 2010, the nation “has announced a target for 2008-12 10% below its commitment under the Kyoto Protocol and a 30% cut compared with 1990 by 2020.” In 2012, EU-15 emissions was 15.1% below their base year level. Based on figures for 2012 by the European Environment Agency, EU-15 emissions averaged 11.8% below base-year levels during the 2008-2012 period. This means the EU-15 over-achieved its first Kyoto target by a wide margin.

Tokyo, Japan

The Japanese city of Tokyo is like a country in its own right in terms of its energy consumption and GDP. Tokyo consumes as much energy as “entire countries in Northern Europe, and its production matches the GNP of the world’s 16th largest country”. A scheme to limit carbon emissions launched in April 2010 covers the top 1,400 emitters in Tokyo, and is enforced and overseen by the Tokyo Metropolitan Government. Phase 1, which is similar to Japan’s scheme, ran until 2015. (Japan had an ineffective voluntary emissions reductions system for years, but no nationwide cap-and-trade program.) Emitters must cut their emissions by 6% or 8% depending on the type of organization; from 2011, those who exceed their limits must buy matching allowances or invest in renewable-energy certificates or offset credits issued by smaller businesses or branch offices. Polluters that fail to comply will be fined up to 500,000 yen plus credits for 1.3 times excess emissions. In its fourth year, emissions were reduced by 23% compared to base-year emissions. In phase 2, (FY2015-FY2019), the target is expected to increase to 15%-17%. The aim is to cut Tokyo’s carbon emissions by 25% from 2000 levels by 2020. These emission limits can be met by using technologies such as solar panels and advanced fuel-saving devices.

United States

Sulfur dioxide

An early example of an emission trading system has been the sulfur dioxide (SO2) trading system under the framework of the Acid Rain Program of the 1990 Clean Air Act in the U.S. Under the program, which is essentially a cap-and-trade emissions trading system, SO2 emissions were reduced by 50% from 1980 levels by 2007. Some experts argue that the cap-and-trade system of SO2 emissions reduction has reduced the cost of controlling acid rain by as much as 80% versus source-by-source reduction. The SO2 program was challenged in 2004, which set in motion a series of events that led to the 2011 Cross-State Air Pollution Rule (CSAPR). Under the CSAPR, the national SO2 trading program was replaced by four separate trading groups for SO2 and NOx. SO2 emissions from Acid Rain Program sources have fallen from 17.3 million tons in 1980 to about 7.6 million tons in 2008, a decrease in emissions of 56 percent. A 2014 EPA analysis estimated that implementation of the Acid Rain Program avoided between 20,000 and 50,000 incidences of premature mortality annually due to reductions of ambient PM2.5 concentrations, and between 430 and 2,000 incidences annually due to reductions of ground-level ozone.[not in citation given]

Nitrogen oxides

In 2003, the Environmental Protection Agency (EPA) began to administer the NOx Budget Trading Program (NBP) under the NOx State Implementation Plan (also known as the “NOx SIP Call”). The NOx Budget Trading Program was a market-based cap and trade program created to reduce emissions of nitrogen oxides (NOx) from power plants and other large combustion sources in the eastern United States. NOx is a prime ingredient in the formation of ground-level ozone (smog), a pervasive air pollution problem in many areas of the eastern United States. The NBP was designed to reduce NOx emissions during the warm summer months, referred to as the ozone season, when ground-level ozone concentrations are highest. In March 2008, EPA again strengthened the 8-hour ozone standard to 0.075 parts per million (ppm) from its previous 0.08 ppm.

Ozone season NOx emissions decreased by 43 percent between 2003 and 2008, even while energy demand remained essentially flat during the same period. CAIR will result in $85 billion to $100 billion in health benefits and nearly $2 billion in visibility benefits per year by 2015 and will substantially reduce premature mortality in the eastern United States. NOx reductions due to the NOx Budget Trading Program have led to improvements in ozone and PM2.5, saving an estimated 580 to 1,800 lives in 2008.[not in citation given]

A 2017 study in the American Economic Review found that the NOx Budget Trading Program decreased NOx emissions and ambient ozone concentrations. The program reduced expenditures on medicine by about 1.5% ($800 million annually) and reduced the mortality rate by up to 0.5% (2,200 fewer premature deaths, mainly among individuals 75 and older).

Volatile organic compounds

In the United States the Environmental Protection Agency (EPA) classifies Volatile Organic Compounds (VOCs) as gases emitted from certain solids and liquids that may have adverse health effects. These VOCs include a variety of chemicals that are emitted from a variety of different products. These include products such as gasoline, perfumes, hair spray, fabric cleaners, PVC, and refrigerants; all of which can contain chemicals such as benzene, acetone, methylene chloride, freons, formaldehyde.

VOCs are also monitored by the United States Geological Survey for its presence in groundwater supply. The USGS concluded that many of the nations aquifers are at risk to low-level VOC contamination. The common symptoms of short levels of exposure to VOCs include headaches, nausea, and eye irritation. If exposed for an extended period of time the symptoms include cancer and damage to the central nervous system.

Greenhouse gases

As of 2017, there is no national emissions trading scheme in the United States. Failing to get Congressional approval for such a scheme, President Barack Obama instead acted through the United States Environmental Protection Agency to attempt to adopt through rulemaking the Clean Power Plan, which does not feature emissions trading. (The plan was subsequently challenged and is under review by the administration of President Donald Trump.)

Concerned at the lack of federal action, several states on the east and west coasts have created sub-national cap-and-trade programs.

State and regional programs

In 2003, New York State proposed and attained commitments from nine Northeast states to form a cap-and-trade carbon dioxide emissions program for power generators, called the Regional Greenhouse Gas Initiative (RGGI). This program launched on January 1, 2009 with the aim to reduce the carbon “budget” of each state’s electricity generation sector to 10% below their 2009 allowances by 2018.

Also in 2003, U.S. corporations were able to trade CO2 emission allowances on the Chicago Climate Exchange under a voluntary scheme. In August 2007, the Exchange announced a mechanism to create emission offsets for projects within the United States that cleanly destroy ozone-depleting substances.

In 2006, the California Legislature passed the California Global Warming Solutions Act, AB-32, which was signed into law by Governor Arnold Schwarzenegger. Thus far, flexible mechanisms in the form of project based offsets have been suggested for three main project types. The project types include: manure management, forestry, and destruction of ozone-depleted substances. However, a ruling from Judge Ernest H. Goldsmith of San Francisco’s Superior Court stated that the rules governing California’s cap-and-trade system were adopted without a proper analysis of alternative methods to reduce greenhouse gas emissions. The tentative ruling, issued on 24 January 2011, argued that the California Air Resources Board violated state environmental law by failing to consider such alternatives. If the decision is made final, the state would not be allowed to implement its proposed cap-and-trade system until the California Air Resources Board fully complies with the California Environmental Quality Act.[needs update] California’s cap-and-trade program ranks only second to the ETS (European Trading System) carbon market in the world. In 2012, under the auction, the reserve price, which is the price per ton of CO2 permit is $10. Some of the emitters obtain allowances for free, which is for the electric utilities, industrial facilities and natural gas distributors, whereas some of the others have to go to the auction.

In 2014, the Texas legislature approved a 10% reduction for the Highly Reactive Volatile Organic Compound (HRVOC) emission limit. This was followed by a 5% reduction for each subsequent year until a total of 25% percent reduction was achieved in 2017.

In February 2007, five U.S. states and four Canadian provinces joined together to create the Western Climate Initiative (WCI), a regional greenhouse gas emissions trading system. In July 2010, a meeting took place to further outline the cap-and-trade system. In November 2011, Arizona, Montana, New Mexico, Oregon, Utah and Washington withdrew from the WCI.

In 1997, the State of Illinois adopted a trading program for volatile organic compounds in most of the Chicago area, called the Emissions Reduction Market System. Beginning in 2000, over 100 major sources of pollution in eight Illinois counties began trading pollution credits.

Failed federal effort

President Barack Obama in his proposed 2010 United States federal budget wanted to support clean energy development with a 10-year investment of US $15 billion per year, generated from the sale of greenhouse gas (GHG) emissions credits. Under the proposed cap-and-trade program, all GHG emissions credits would have been auctioned off, generating an estimated $78.7 billion in additional revenue in FY 2012, steadily increasing to $83 billion by FY 2019. The proposal was never made law.

The American Clean Energy and Security Act (H.R. 2454), a greenhouse gas cap-and-trade bill, was passed on 26 June 2009, in the House of Representatives by a vote of 219-212. The bill originated in the House Energy and Commerce Committee and was introduced by Representatives Henry A. Waxman and Edward J. Markey. The political advocacy organizations FreedomWorks and Americans for Prosperity, funded by brothers David and Charles Koch of Koch Industries, encouraged the Tea Party movement to focus on defeating the legislation. Although cap and trade also gained a significant foothold in the Senate via the efforts of Republican Lindsey Graham, Independent and former Democrat Joe Lieberman, and Democrat John Kerry, the legislation died in the Senate.

South Korea

South Korea’s national emissions trading scheme officially launched on 1 January 2015, covering 525 entities from 23 sectors. With a three-year cap of 1.8687 billion tCO2e, it now forms the second largest carbon market in the world following the EU ETS. This amounts to roughly two-thirds of the country’s emissions. The Korean emissions trading scheme is part of the Republic of Korea’s efforts to reduce greenhouse gas emissions by 30% compared to the business-as-usual scenario by 2020.

China

Pollution Permit Trading

In an effort to reverse the adverse consequences of air pollution, in 2006, China started to consider a national pollution permit trading system in order to use market-based mechanisms to incentivize companies to cut pollution. This has been based on a previous pilot project called the Industrial SO2 emission trading pilot scheme, which was launched in 2002. Four provinces, three municipalities and one business entity was involved in this pilot project (also known as the 4+3+1 project). They are Shandong, Shanxi, Jiangsu, Henan, Shanghai, Tianjin, Liuzhou and China Huaneng Group, a state-owned company in the power industry. This pilot project did not turn into a bigger scale inter-provincial trading system, but it stimulated numerous local trading platforms.

In 2014, when the Chinese government started considering a national level pollution permit trading system again, there were more than 20 local pollution permit trading platforms. The Yangtze River Delta region as a whole has also run test trading, but the scale was limited. In the same year, the Chinese government proposed establishing a carbon market, focused on CO2 reduction later in the decade, and it is a separate system from the pollution permit trading.

Carbon Market

China currently emits about 30% of global emission, and it became the largest emitter in the world. When the market launched, it will be the largest carbon market in the world. The initial design of the system targets a scope of 3.5 billion tons of carbon dioxide emissions that come from 1700 installations. It has made a voluntary pledge under the UNFCCC to lower CO2 per unit of GDP by 40 to 45% in 2020 when comparing to the 2005 levels.

In November 2011, China approved pilot tests of carbon trading in seven provinces and cities – Beijing, Chongqing, Shanghai, Shenzhen, Tianjin as well as Guangdong Province and Hubei Province, with different prices in each region. The pilot is intended to test the waters and provide valuable lessons for the design of a national system in the near future. Their successes or failures will, therefore, have far-reaching implications for carbon market development in China in terms of trust in a national carbon trading market. Some of the pilot regions can start trading as early as 2013/2014. National trading is expected to start in 2017, latest in 2020.

The effort to start a national trading system has faced some problems that took longer than expected to solve, mainly in the complicated process of initial data collection to determine the base level of pollution emission. According to the initial design, there will be eight sectors that are first included in the trading system, chemicals, petrochemicals, iron and steel, non-ferrous metals, building materials, paper, power and aviation, but many of the companies involved lacked consistent data. Therefore, by the end of 2017, the allocation of emission quotas have started but it has been limited to only the power sector and will gradually expand, although the operation of the market is yet to begin. In this system, Companies that are involved will be asked to meet target level of reduction and the level will contract gradually.

India

Trading is set to begin in 2014 after a three-year rollout period. It is a mandatory energy efficiency trading scheme covering eight sectors responsible for 54 per cent of India’s industrial energy consumption. India has pledged a 20 to 25 per cent reduction in emissions intensity from 2005 levels by 2020. Under the scheme, annual efficiency targets will be allocated to firms. Tradable energy-saving permits will be issued depending on the amount of energy saved during a target year.

Renewable energy certificates

Renewable Energy Certificates (occasionally referred to as or “green tags” [citation required]), are a largely unrelated form of market-based instruments that are used to achieve renewable energy targets, which may be environmentally motivated (like emissions reduction targets), but may also be motivated by other aims, such as energy security or industrial policy.

Source from Wikipedia